Diversification is the only free lunch in investing—it reduces risk without lowering expected returns. Yet many investors make diversification mistakes that leave their portfolio vulnerable. In this guide, you'll learn how to diversify correctly.

What is Diversification?

Diversification means spreading your investment across different assets, sectors, and geographies so that poor performance in one area doesn't destroy your entire portfolio.

Simple example: All-in on 1 tech stock = risky. 50 stocks across 10 sectors = diversified.

Why Diversify?

1. Reduce Risk

If one company goes bankrupt but you hold 50 companies, you lose 2%, not 100%.

2. Smooth Returns

If tech drops but utilities rise, your portfolio stays stable.

3. Psychological Peace

Less anxiety during crashes—you know your portfolio will survive.

4. Sleep Better

All-in crypto = lying awake. Diversified portfolio = sleeping soundly.

How to Diversify?

1. Asset Class Diversification

- Stocks: 60-70% (growth engine)

- Bonds: 20-30% (stability)

- Real Estate/REITs: 5-10% (inflation hedge)

- Commodities/Gold: 5-10% (safe haven)

- Cash: 5-10% (opportunities + emergency)

2. Sector Diversification

Spread across sectors:

- Technology

- Healthcare

- Financials

- Consumer (Staples & Discretionary)

- Industrials

- Energy

- Utilities

- Materials

- Real Estate

No sector should exceed 25% or your equity portfolio.

3. Geographic Diversification

- US: 40-50% (largest economy)

- Europe: 20-25%

- Emerging markets: 10-20%

- Asia: 10-15%

4. Company Size Diversification

- Large cap: 60-70% (stability)

- Mid cap: 20-30% (growth potential)

- Small cap: 10% (high growth, but also high risk)

How Many Stocks is Enough?

Research shows that most diversification benefit comes from the first 15-20 stocks. After that, additional diversification is marginal.

- 5 stocks: Insufficient—too concentrated

- 15-20 stocks: Sweet spot—good diversification without overdoing it

- 50+ stocks: Over-diversification—difficult to manage, returns drop toward market average

False Diversification

Mistake 1: Ignoring Correlation

"I have 10 stocks"—but all tech = not diversified. Apple, Microsort, Google orten crash together.

Mistake 2: Home Bias

"Only Dutch stocks"—you're overexposed to one economy. The Netherlands is 0.5% or world market cap.

Mistake 3: Recency Bias

"Tech did well, I'm going all-in tech"—exactly when the sector is overbought.

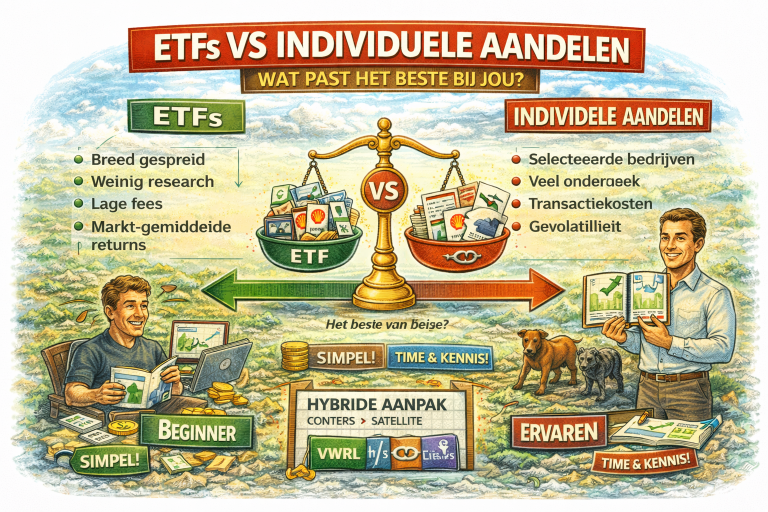

Simple Diversification with ETFs

For lazy investors:

- 100% VWRL (World Index ETF) = instant diversification across 3900+ companies

- Or: 88% IWDA (Developed) + 12% EMIM (Emerging)

For a bit more control:

- 60% VWRL (stocks)

- 30% Bond ETF

- 10% Gold/Commodities ETF

Rebalancing

Over time, your allocation shifts. Tech does well → now 80% tech = too concentrated.

Rebalance strategy:

- Check allocation each quarter

- If sector/asset is > 10% above target: sell excess

- Reinvest in underweight areas

- Or: new contributions go to underweight assets

Life Stage Diversification

Young (20-35):

- 80-90% stocks

- 10-20% bonds

- Can take risk—long time horizon

Mid-career (35-50):

- 70-80% stocks

- 20-30% bonds/fixed income

Pre-retirement (50-65):

- 60-70% stocks

- 30-40% bonds

- More stability

Retirement (65+):

- 40-50% stocks

- 50-60% bonds/cash

- Capital preservation focus

For more on diversification, check out Investopedia's diversification guide.

Conclusion

Diversification is essential but requires balance. Too little = unnecessary risk. Too much = diluted returns and management nightmare. For most investors, 15-20 stocks across different sectors + countries is ideal. Or even simpler: one global index ETF gives instant perfect diversification. Start there, add more later if you want. The key is: think about correlations, spread risk, and review regularly. Diversification isn't a one-time decision but an ongoing process.